Yesterday, the Bank of Japan increased its policy target rate for the first time in…

Japan needs to abandon its reliance on export growth

The economic news yesterday from Japan that the economy had contracted in the second-quarter 2015 by 0.4 per cent (Real GDP) on the back of a sharp drop in exports (-4.4 per cent) and private consumption (-0.8 per cent). The economy is 0.7 per cent larger in real terms than this time last year but that is somewhat misleading because of the 1.9 per cent decline in the June-quarter 2014 after the Government introduced its latest sale tax hike fiasco. The only positive contributors to growth in the June-quarter 2015 were inventories and the public sector (both consumption and investment). The continuing declines in real wages and pessimistic consumer expectations are undermining the capacity of the private domestic sector to sustain growth. Without the growth in public spending the quarterly decline in real GDP growth would have been much worse. It is likely that the slowdown in China is impacting negatively on Japanese exports. But with China trying to stabilise around a mean-shift downwards in its growth rate, the future for all export-led growth strategies (that have been relying on China to sustain much higher rates of growth) doesn’t look good. In the same way that China appears to be rebalancing its total output in favour of domestic spending, the same strategy should be adopted by Japan to wean itself of its reliance on continued strong growth in exports. One thing that Japan might re-assess is its – National Pension Scheme – which is not only fairly meagre in income payments but also forces workers to contribute during their working lives. Given Japan is a currency-issuing nation, it could easily increase the pension payment and reduce or eliminate the contribution, thus providing more certainty to workers in retirement.

The thrust of Abeconomics was that Japan would achieve sustained growth via a renewed export boom.

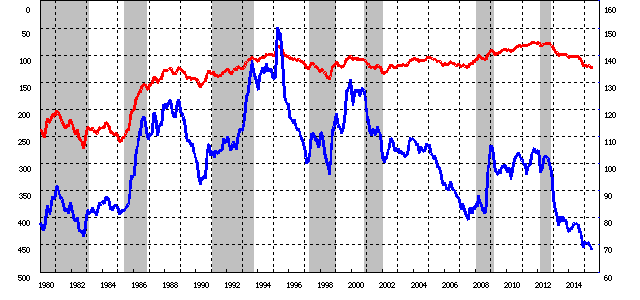

Japan’s exchange rate has depreciated significantly in the last 3 years or so. Since October 2011 (its most recent peak – 76.72 Yen per US dollar), the Yen has depreciated by some 60 per cent against the US dollar (in July, 123.3 Yen per US dollar).

The following graph (from the BOJ) shows the monthly US dollar to Yen parity and also the real effective exchange rate, which is a measure of international competitiveness.

Real effective exchange rates provide a measure on international competitiveness and are based on information pertaining movements in relative prices and costs, expressed in a common currency.

For an explanation of the REER and its interpretation, please read this blog – Time to ditch the export-led growth mania.

If the REER rises, then we conclude that the nation is less internationally competitive and vice-versa. The real exchange rate is the blue line graphed on the right-hand axis.

Note the left-hand axis (the nominal exchange rate) is reversed, so a decline in the red line indicates that more US dollars exchange for one yen.

It makes you wonder what the scaremongering about depreciating currencies is all about – for example, the claims that a catastrophe would follow if Greece floated its exchange rate upon exit.

Here is an advanced nation engineering a massive depreciation of its exchange rate to gain competitive edge in international trade.

The Japanese did the same thing in the late 1990s. A well established understanding is that Japan’s trade sector is fairly responsive to exchange rate movements and that the current account surplus rises when the Yen depreciates, which through the income effects of increased net exports adds to growth.

The depreciation reflects the decisions by the Bank of Japan to expand its bond-buying purchases.

But the other point is that the Yen to the Chinese Yuan rate has not depreciated over the last 4 months and in the recent period has appreciated quite sharply.

What have been the impacts on real GDP through trade?

Japanese net exports have grown strongly from the middle of last year, which has attenuated, to some degree, the negative impact of the sales tax rise on household consumption.

However, export growth was sharply negative in the June-quarter 2015 while imports also fell.

So mixed outcomes. Clearly, in the June-quarter 2015, the external sector drained economic growth in Japan (by 0.4 percentage points).

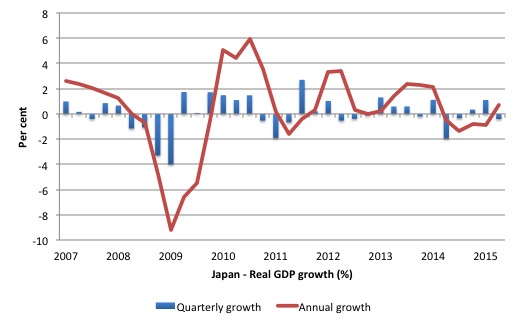

The following graph shows the growth of real GDP from the March-quarter 2007 to the June-quarter 2015. The annual growth (year-on-year) is in blue bars while the red line is the quarterly growth rate.

On an annual basis, Japan came out of recession in the June-quarter, with the latest annual growth rate of 0.7 per cent, driven by the two-quarters of positive growth prior to June-quarter 2015.

The sudden negative spike in the June-quarter 2014 result was the direct outcome of neo-liberal incompetence (the sales tax hike) and is no longer affecting the annualised growth rate calculation.

But the quarterly result for the June-quarter 2015 is a bad sign.

The latest – Consumer Confidence Survey – published by the Cabinet Office (August 10, 2015) showed that:

1. The index was down 1.4 percentage points in July from June 2015.

2. All components of the index fell in July (overall livelihood, -1.3 points; income growth, -0.7 points; employment, -2.6 points) and willingness to buy durable goods, -1.1 points).

So household consumption expenditure is looking decidedly weak as the impacts of the sales tax hike remains negative and the negative export growth impinges on employment and income growth.

The Abe government raised the sales tax from 5 per cent to 8 per cent in April 2014 as part of a ridiculous plan to reduce the fiscal deficit.

Japan then endured 4 successive quarters of negative growth in household consumption. Domestic demand is now 2.1 per cent lower than it was in the March-quarter 2014, prior to the imposition of the sales tax hike.

Please read my blog – Japan returns to 1997 – idiocy rules! – for more discussion on the damaging impacts of sales tax hikes.

Private consumption has still not recovered from the sales tax increase in April last year. It is still 4.8 per cent below the level enjoyed in the March-quarter 2014.

The sales tax hike was a replay of the events that occurred in 1997 when the ideologues came out in force and pressured the national government to cut into the fiscal deficit.

The government raised the sales tax then with disastrous consequences. The lessons clearly have not been learned.

I discussed the 1997 debacle in detail in this blog – Japan thinks it is Greece but cannot remember 1997

The direct impact on private consumption of the 1997 sales tax hike have been replicated in 2014 into 2015.

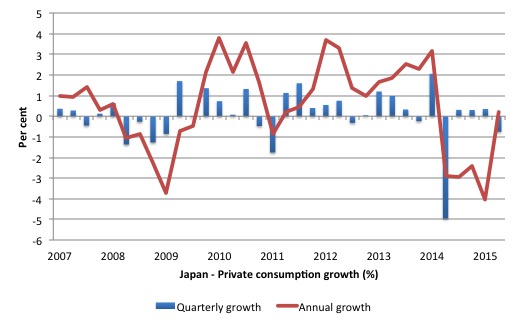

The following graph shows growth in private consumption spending since the March-quarter 2007. The blue bars are the annual (year-on-year) outcome, while the red line is the quarterly result.

This is one of those magnificent graphs that you show students to demonstrate intervention effects of government policy. Private consumption growth was growing fairly strongly on up to the beginning of 2014, after the impacts of the GFC and the Tsunami had been overcome.

The sales tax hike had the predictable negative effect with a sudden dive in consumption overall in the June-quarter 2014 (-5.0 per cent) followed by three quarters of tepid growth (0.3 per cent in each).

The combination of the sales tax hike, declining real wages, and the export decline have caused the quarterly growth of private consumption to decline again in the June-quarter 2015 (-0.8 percent), which has all but wiped out the gains made since the March-quarter 2014.

It is hard to construe the data as telling us that private consumption in Japan is going to drive growth any time soon under the current policy settings.

In this blog written in September 2014 – Japan’s growth slows under tax hikes but the OECD want more – I predicted that:

The drop in private consumption spending is a direct result of the sales tax hike. It will get worse.

It was obvious that the economy would deteriorate further.

First, consumers stopped spending (last quarter) and then adopted a very cautious approach. In part, this is because real wages have been falling consistently for some quarters now (see below).

The impact of static consumption expenditure is that business investment then lags.

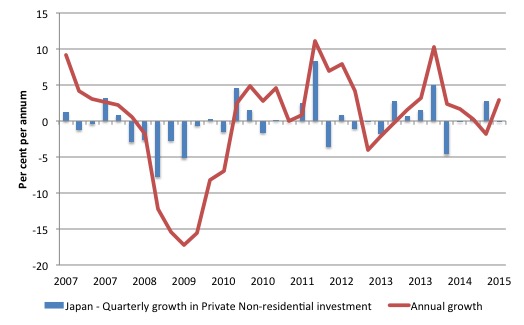

The following graph shows the quarterly (blue bars) and annual growth (red line) in private investment from the March-quarter 2007 to the June-quarter 2015.

The positive result in the current quarter is down to the blip in the March-quarter 2015. In the June-quarter 2015, Private investment (non-residential) was slightly negative.

Not a glowing outlook.

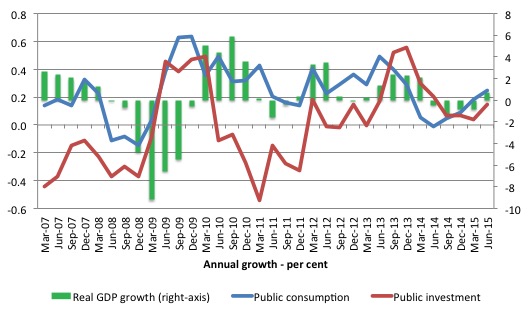

The next graph shows, there was a strong counter-cyclical fiscal response in both public consumption and investment over this period of private spending decline.

The government started withdrawing its fiscal stimulus too early – even though growth in government consumption continued through 2010 as public investment started to contract. While the non-government components of spending were starting to recover they were not strong enough to resist the slowing fiscal impact and so real GDP growth started to moderate.

The fiscal response in the last four quarters has been strong. Public consumption grew by 1.3 per cent in the June-quarter 2015 while public investment grew by 3.4 per cent. Both components of public spending thus contributed positively to overall growth, to partially offset the decline in the non-government sector spending.

If the Abe government had have taken the advice of the IMF and OECD which were both hectoring Japan to reduce its public spending then the current situation in Japan would have been much worse than it is.

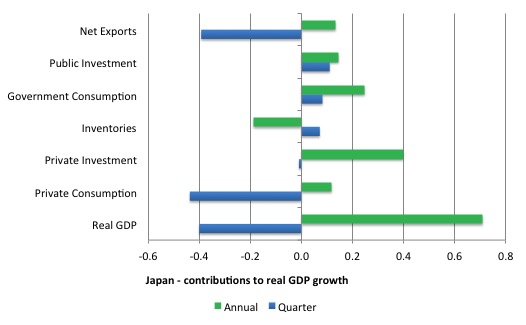

The next graph shows the contributions (in percentage points) to real GDP growth of the major expenditure categories in Japan over the last quarter and over the last 12 months (to the June-quarter 2015).

It is also clear that over the last year, the external sector has contributed to growth but that contribution turned sharply negative in the June-quarter 2015.

It is also clear that the public sector has been a major contributor to growth over the last 12 months and continued to prop it up in the recent quarter.

The spending behaviour of the non-government sector is clearly undermining overall growth in Japan.

Real wages have been falling in Japan for some time, which has acted to suppress consumption spending.

The Japanese Ministy of Health, Labour and Welfare publishes a Monthly Labour Survey. The latest data on – Total Cash Earnings provides some information on wage movements.

The following graph shows the movement in the All Industries Wage Index since 2011 (the first six months of 2015 are averaged to give the 2015 result) and the CPI index since 2011 (red line).

The series are indexed to 100 at 2011. The real wage index now stands at 93.4 while the price level index stands at 103.3.

Real wages have thus fallen by about 10 per cent in four year – a substantial drop.

Taken together, we learn from most recent data that:

1. Fiscal policy works in both directions – trying to cut deficits will reduce economic growth (and vice versa) – when the economy is below full employment.

2. Monetary policy does little to stimulate real spending in a monetary economy and can not offset contractionary movements in fiscal policy. The Bank of Japan has been engaging in more quantitative easing and interest rates remain around zero – but there has so far been very little real GDP impact.

What does this mean for the current policy strategy in Japan?

First, the export-led growth strategy is being undermined by the slowdown in China, which is Japan’s largest export market.

China has woken up to the fact that the strategy that worked for South Korea (as an example) is not going to endure into the next decade or more.

China is trying to redirect total activity towards domestic demand, even as it deliberately realigns its currency to help its declining export sector.

There is a misperception that the Chinese export sector has been the strongest driver of growth. There is only limited truth in that belief.

Net exports contributed negatively to growth in China in 2009, were a zero contribution in 2010, plunged again in 2011, rebounded in 2012, derailed growth in 2013, and contributed strongly in 2014.

But overall, there has been a substantial shift towards domestic spending as the roller coaster external sector moderated its overall contribution.

Japan should follow this example and understand that China will increasingly shift its overall economic activity into domestic services production (as any mature economy does).

Further depreciation in the Yen will not particularly help, especially as China is also realigning its currency downwards. The income effects from the slower Chinese growth will swamp the price effects arising from any depreciation in the yen anyway.

The Japanese government has to maintain strong fiscal support for domestic demand to improve the household and firm confidence.

There is a case to be made for widespread pension reform to take the responsibility off the private sector to fund their own retirements and, instead, increase the public contribution for retirement incomes. That would help boost private consumption growth.

But there is also a burning need to stimulate wages growth, which is a major reason why consumption growth is so flat (and negative this quarter).

Conclusion

When the Japanese government announced its staggered sales tax hikes, any sensible person would have concluded that just as in 1997, the economy would head south.

It did.

All those claims by the OECD and the IMF, among others that the Japanese government had to increase sales taxes to raise more government revenue were just the ravings on vandals.

There is no such thing as “growth-friendly” fiscal austerity.

Japan is now in danger of plunging back into recession as the slowdown in Chinese economic growth undermines Japan’s export markets and real wage cuts undermine private domestic spending.

With declining real wages and consumer sentiment, the Japanese government would do well to stimulate domestic spending by increasing public spending in the first instance and boosting private employment growth.

Upcoming Event – Reframing the Debate: Economics for a Progressive Politics, London, August 27, 2015

The organisers of the following event have found a new venue and those who missed out on seats who want to attend can now register and receive tickets.

The NHA is very pleased to be able to present an evening with Professor Bill Mitchell, Professor of Economics and renowned proponent of Modern Monetary Theory, during his visit to the UK at the end of this month.

Come and join Professor Mitchell in conversation with Richard Murphy (Tax Research) and Ann Pettifor (Prime Economics), both currently economic advisors to Jeremy Corbyn’s campaign.

How can the debate on the economy be reframed around the things that really matter – people and the environment? Does MMT hold the key?

This is sure to be a fascinating debate.

The Event will be held on Thursday, August 27, 2015 from 18:30 to 20:30 (BST).

The location:

John Snow Theatre

London School of Hygiene and Tropical Medicine

Keppel Street

WC1E 7HT London

United Kingdom

WWW site for Registration.

The event is free and all are welcome.

Upcoming Event – Book Launch Maastricht, August 31, 2015

The official book launch for my new book – Eurozone Dystopia – Groupthink and Denial on a Grand Scale – will be held on Monday, August 31, 2015 at the Maastricht University, the Netherlands.

The Launch will be held at the SBE Building, Tongersestraat 53, Maastricht University. The Room will be announced in due course.

The event will run from 13:00 to 14:30 and there will be two excellent speakers:

1. Dr László Andor, former Commissioner for Employment, Social Affairs and Inclusion in the Barroso II administration of the European Commission.

2. Professor Arjo Klamer, Professor of Economics of Art and Culture at Erasmus University in Rotterdam, The Netherlands. He “holds the world’s only chair in the field of cultural economics”.

The public is welcome to the event and there will refreshments available. I hope to see a lot of people there in Maastricht on August 31.

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

Bill

I wonder if there is any chance that there will be a recording of the debate you are going to at the end of the month and if it will be put on the web? It would be really useful to hear the debate, but there is no chance of getting to London to attend.

Thanks

Dear Bill

Japan’s aging population demands that there will be a greater need for geriatric services, which aren’t imported and therefore don’t have to be financed by imports. Japan’s shrinking population means that its need for imports will be lower, at a given level of per capita income, which is another reason why exports don’t need to grow. When analyzing Japan, we should always bear in mind that it is a country with below-replacement fertility and little immigration, therefore a country with a declining population.

Regards. James

Bill,

Will you discuss the Job Guarantee during your meeting with Murphy and Pettifor?

Richard1, I have been informed that a film about MMT is being made and is supposed to include the 27 August debate. I have no idea how much of Bill’s or the other panelists’ presentations will be broadcast, unfortunately.

Larry

Many thanks, I’ll look out for it

Richard1,

The organisers are in discussion with the documentary makers to find out if the debate can also be filmed and uploaded to YouTube seperately.

I’ve haven’t heard anything further so far..

Mike

Many thanks – it would be great if it happened

Thanks for this post.

Mini-question: from what I’ve read in the last weeks, the Chinese government seems to try and motivate private spending by encouraging stock bubbles. Is this actually true and have they not learned from the US experience or are those symptoms of something else?

The organisers have both told me that the London meeting will be recorded and uploaded onto You Tube in full. There is also a documentary being recorded by Sky, which will contain edited highlights.

To all

There is some misinformation about the filming at the MMT event in London next week.

A British film maker has been doing a documentary on MMT for some time and had arranged to do some filming with me while I was in Europe this year. When it became clear that a public event could be organised for the period I was in London, I invited the film maker to come along. We are doing some separate filming outside of the event.

Once that was arranged, it then became possible to upload his footage onto YouTube for all to see. As far as I know this exercise is not a Sky TV documentary. That might have been negotiated independently of the other arrangements.

best wishes

bill